Understanding Tax Deductions and Credits to Lower Your Bill

Maximize your tax savings by understanding and utilizing available tax deductions and credits.

Maximize your tax savings by understanding and utilizing available tax deductions and credits. Let's dive deep into how you can keep more of your hard-earned money by smartly navigating the world of tax deductions and credits. It's not just about filing your taxes; it's about optimizing them! Many people leave money on the table simply because they don't know what they're eligible for. This guide will break down everything you need to know, from common deductions to powerful credits, and even recommend some tools to help you along the way.

Understanding Tax Deductions and Credits to Lower Your Bill

What are Tax Deductions and How Do They Reduce Your Taxable Income

First things first, let's clarify what a tax deduction is. Think of a deduction as something that reduces your taxable income. It's not a dollar-for-dollar reduction in your tax bill, but rather a reduction in the amount of income the government considers taxable. For example, if you earn $50,000 and have $5,000 in deductions, your taxable income drops to $45,000. This means you'll pay taxes on $45,000 instead of $50,000, which can lead to significant savings, especially if it pushes you into a lower tax bracket. The more deductions you can claim, the lower your taxable income, and ultimately, the less tax you owe.

There are two main types of deductions: the standard deduction and itemized deductions. You generally choose one or the other, whichever results in a lower taxable income for you. The standard deduction is a fixed dollar amount set by the IRS that you can subtract from your adjusted gross income (AGI). It varies based on your filing status (single, married filing jointly, head of household, etc.) and whether you're over 65 or blind. For instance, for the 2023 tax year, the standard deduction for a single filer was $13,850. If your total itemized deductions don't exceed this amount, taking the standard deduction is usually the simpler and more beneficial option.

Itemized deductions, on the other hand, are specific expenses you can subtract from your AGI. These include things like state and local taxes (SALT), mortgage interest, medical expenses (if they exceed a certain percentage of your AGI), charitable contributions, and more. You'd typically itemize if your total eligible expenses are greater than the standard deduction. Keeping meticulous records of these expenses throughout the year is crucial if you plan to itemize. We'll dive into some common itemized deductions in a bit.

Exploring Common Tax Deductions for Individuals and Families

Let's get into some of the most common deductions that many individuals and families can take advantage of. Knowing these can really make a difference in your tax outcome.

Student Loan Interest Deduction: Saving on Education Costs

If you're paying off student loans, you might be able to deduct the interest you paid. This deduction can be up to $2,500 or the amount of interest you actually paid, whichever is less. It's an 'above-the-line' deduction, meaning you can claim it even if you take the standard deduction. This is a big win for many people burdened by student loan debt.

IRA Contributions: Boosting Retirement and Lowering Taxes

Contributing to a traditional IRA can be a fantastic way to save for retirement and reduce your current tax bill. The amount you can deduct depends on your income, whether you're covered by a retirement plan at work, and your filing status. For 2023, the maximum contribution was $6,500 ($7,500 if you're 50 or older). This deduction is also 'above-the-line,' making it accessible to more taxpayers.

Health Savings Account HSA Contributions: Triple Tax Advantage

If you have a high-deductible health plan (HDHP), you might be eligible for an HSA. Contributions to an HSA are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. It's often called a 'triple tax advantage' and is an excellent way to save for healthcare costs while reducing your taxable income. For 2023, the maximum contribution for an individual was $3,850 and for a family was $7,750.

Self Employment Tax Deduction: For the Entrepreneurs

If you're self-employed, you pay both the employer and employee portions of Social Security and Medicare taxes. The good news is you can deduct one-half of your self-employment taxes from your gross income. This helps offset the additional tax burden on freelancers and small business owners.

Itemized Deductions Deep Dive: Mortgage Interest, Charitable Giving, and Medical Expenses

For those who itemize, these are some of the big ones:

- Mortgage Interest: You can deduct the interest paid on your home mortgage, up to certain limits. This is often a significant deduction for homeowners.

- State and Local Taxes (SALT): This includes property taxes, state income taxes, or state sales taxes. However, there's a cap of $10,000 per household for this deduction, which has been a point of contention for many taxpayers in high-tax states.

- Charitable Contributions: Donations to qualified charities can be deducted. You'll need proper documentation, especially for larger donations. For cash contributions, you can generally deduct up to 60% of your AGI, and for non-cash contributions, it's usually 50% or 30% depending on the type of property and organization.

- Medical and Dental Expenses: You can deduct the amount of medical and dental expenses that exceeds 7.5% of your adjusted gross income. This threshold means it's often difficult to claim unless you have very high medical costs.

Understanding Tax Credits and Their Direct Impact on Your Tax Bill

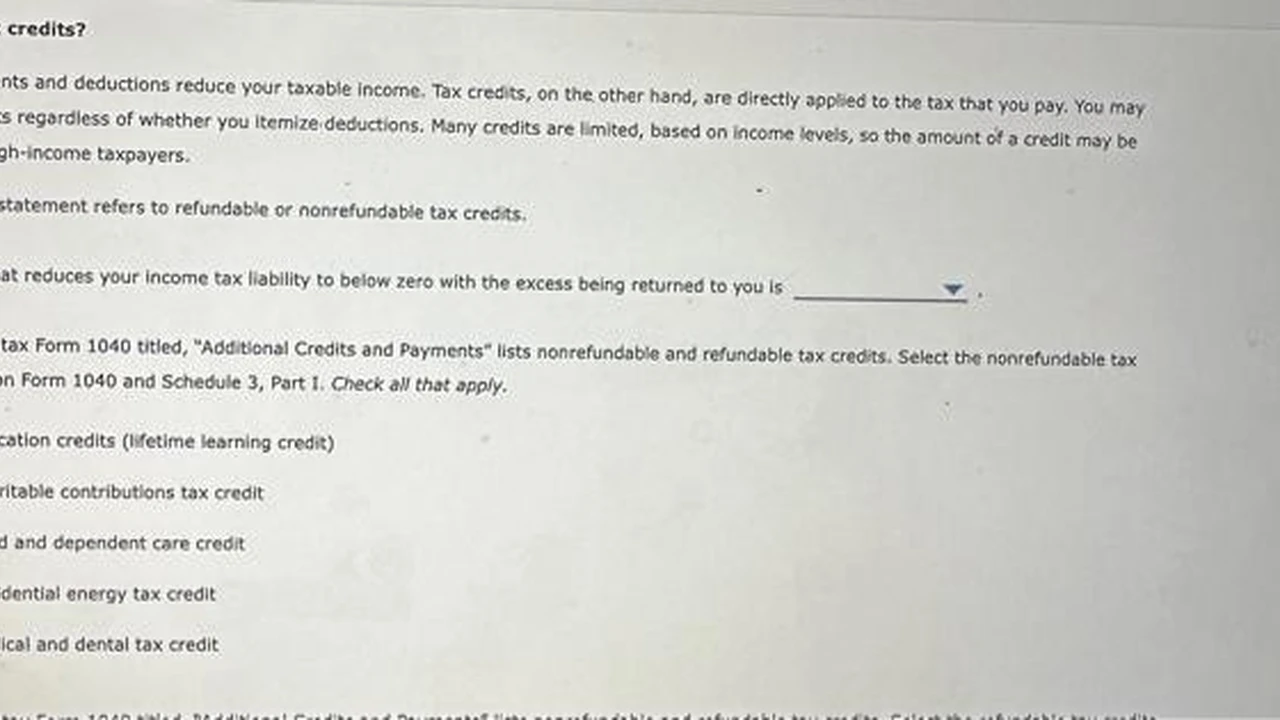

Now, let's talk about tax credits. If deductions reduce your taxable income, credits are even better: they directly reduce your tax bill, dollar for dollar! A $1,000 credit means $1,000 less in taxes you have to pay. This is why credits are often more powerful than deductions. There are two main types of credits: refundable and non-refundable.

Non-refundable credits can reduce your tax liability to zero, but you won't get any money back if the credit amount exceeds your tax bill. Refundable credits, on the other hand, can reduce your tax liability below zero, meaning you could get a refund even if you didn't owe any taxes to begin with. Understanding which credits you qualify for is key to maximizing your refund or minimizing what you owe.

Exploring Powerful Tax Credits for Individuals and Families

Let's look at some of the most impactful tax credits available.

Child Tax Credit CTC: A Major Boost for Families

The Child Tax Credit is a big one for families with qualifying children. For 2023, it's worth up to $2,000 per qualifying child, with up to $1,600 of that being refundable. This means many families can receive a significant refund even if they don't owe much in taxes. The child must be under age 17 at the end of the tax year and meet other dependency tests.

Earned Income Tax Credit EITC: Supporting Low to Moderate Income Workers

The EITC is a refundable credit designed to help low to moderate-income working individuals and families. The amount of the credit depends on your income, filing status, and the number of qualifying children you have. It can be a substantial credit, sometimes thousands of dollars, and is a major source of refunds for eligible taxpayers. The IRS has an EITC Assistant tool on their website to help you determine if you qualify.

Child and Dependent Care Credit: Helping Working Parents

If you pay for childcare so you can work or look for work, you might qualify for this credit. It's a non-refundable credit that can help offset the costs of daycare, after-school programs, and other care for children under 13 or dependents who can't care for themselves. The amount of the credit depends on your income and the amount of expenses you incur, up to a maximum of $3,000 for one qualifying person or $6,000 for two or more.

Education Credits: American Opportunity and Lifetime Learning

There are two main education credits to help with college costs:

- American Opportunity Tax Credit (AOTC): This credit is for eligible students in their first four years of higher education. It's worth up to $2,500 per student, and 40% of it is refundable. You can claim it for tuition, fees, and course materials.

- Lifetime Learning Credit (LLC): This credit is for students taking courses towards a degree or to acquire job skills. It's worth up to $2,000 per tax return (not per student) and is non-refundable. It's more flexible than the AOTC as it doesn't have a limit on the number of years it can be claimed.

Retirement Savings Contributions Credit Saver's Credit: Rewarding Savers

This credit is for low to moderate-income taxpayers who contribute to an IRA or employer-sponsored retirement plan. It's a non-refundable credit that can be worth up to $1,000 for individuals or $2,000 for married couples filing jointly. The amount of the credit depends on your AGI and contribution amount, and it's designed to encourage retirement savings.

Clean Energy Credits: Investing in a Greener Future

With a focus on sustainability, there are several credits available for making energy-efficient home improvements or purchasing clean energy vehicles. These include the Residential Clean Energy Credit (for solar panels, wind turbines, etc.) and credits for new and used clean vehicles. These can be substantial and are a great way to save money while helping the environment.

Comparing Deductions vs Credits Which is More Beneficial for Your Tax Situation

So, which is better: deductions or credits? In most cases, credits are more beneficial because they directly reduce your tax bill dollar for dollar. A $1,000 credit saves you $1,000 in taxes, regardless of your tax bracket. A $1,000 deduction, on the other hand, only saves you your tax bracket percentage of $1,000. For example, if you're in the 22% tax bracket, a $1,000 deduction saves you $220.

However, that doesn't mean deductions aren't important. They can significantly lower your taxable income, potentially pushing you into a lower tax bracket, which then means all your income is taxed at a lower rate. The best strategy is to claim all eligible deductions and credits. You don't have to choose one over the other; you can often benefit from both!

The key is to understand what you qualify for and to keep excellent records. Many people miss out on savings because they don't track their expenses or aren't aware of all the available tax breaks.

Essential Tools and Software for Maximizing Your Tax Savings

Navigating deductions and credits can feel overwhelming, but thankfully, there are some fantastic tools and software out there to help. These products can guide you through the process, identify potential savings, and even file your taxes for you.

TurboTax: User Friendly Tax Preparation Software

Product: TurboTax Use Case: Ideal for individuals and families with varying levels of tax complexity, from simple W-2 filers to those with investments, self-employment income, or rental properties. It's known for its user-friendly interface and step-by-step guidance. Comparison: TurboTax excels in its intuitive interview-style process, making it easy for even novice filers to understand. It asks plain-language questions and helps you uncover deductions and credits you might not have known about. It often integrates well with financial institutions to import data. Pricing: TurboTax offers several versions. The Free Edition (for simple returns) is $0. Deluxe (for itemized deductions, child tax credit, etc.) typically starts around $60 for federal, plus state fees. Premier (for investments, rental property) is around $90+. Self-Employed (for freelancers, small business owners) is around $120+. Prices can vary and often have promotional discounts, especially early in the tax season. They also offer live expert help for an additional fee.

H&R Block: Comprehensive Support and Tax Expertise

Product: H&R Block Tax Software Use Case: Similar to TurboTax, H&R Block caters to a wide range of taxpayers. They also have a strong presence with physical offices, offering in-person support if you prefer that over purely online tools. Comparison: H&R Block's software is also very user-friendly, with a clear interview process. Many users find its interface slightly more traditional than TurboTax, but equally effective. A key differentiator is their extensive network of tax professionals available for in-person assistance or online review of your return. They often have competitive pricing and guarantees. Pricing: H&R Block's online versions typically start with a Free Online option for simple returns. Deluxe (for itemized deductions, HSA, etc.) is usually around $55 for federal, plus state. Premium (for investments, rental income) is around $75+. Self-Employed is around $110+. Like TurboTax, prices are subject to change and promotions. They also offer 'Tax Pro Review' services for an additional cost.

TaxAct: Budget Friendly Option for Savvy Filers

Product: TaxAct Use Case: A great option for those who are comfortable with tax concepts and want a more budget-friendly solution. It's suitable for most common tax situations, including investments and self-employment, but might require a bit more self-direction than TurboTax or H&R Block. Comparison: TaxAct is often praised for its lower price point while still offering robust features. It provides a good balance between cost and functionality. While it might not hold your hand quite as much as the premium options, it's perfectly capable of handling complex returns and identifying deductions and credits. Its interface is clean and efficient. Pricing: TaxAct typically offers a Free option for simple returns. Deluxe (for itemized deductions, dependents) is often around $30 for federal, plus state. Premier (for investments, rental property) is around $45+. Self-Employed is around $65+. These prices are generally lower than competitors, making it an attractive choice for cost-conscious filers.

FreeTaxUSA: Truly Free Federal Filing

Product: FreeTaxUSA Use Case: Excellent for anyone looking to file their federal taxes for free, regardless of complexity. It supports all major forms and schedules, including those for self-employment, investments, and rental income. State filing is available for a small fee. Comparison: The biggest draw for FreeTaxUSA is its genuinely free federal filing. Unlike some 'free' versions of other software that limit features, FreeTaxUSA offers comprehensive federal filing for $0. This makes it a standout for those who want to save on preparation fees. The interface is functional and straightforward, though perhaps not as polished as TurboTax or H&R Block. It's a no-frills, highly effective option. Pricing: Federal filing is $0. State filing is typically around $14.99 per state. They also offer a Deluxe Edition for a small fee (around $7.99) which includes priority support and audit assistance, but it's not necessary for filing.

Quicken Simplifi or Mint: For Year Round Financial Tracking

Product: Quicken Simplifi / Mint (now part of Credit Karma) Use Case: While not tax software themselves, these financial tracking apps are invaluable for organizing your financial life throughout the year, which directly impacts your ability to claim deductions and credits. They help you categorize expenses, track income, and monitor investments. Comparison: Simplifi and Mint both offer robust budgeting, spending tracking, and net worth monitoring. They connect to your bank accounts, credit cards, and investment accounts to give you a holistic view of your finances. Mint has historically been free (ad-supported), while Simplifi is a subscription service. Having well-categorized expenses makes tax preparation much faster and ensures you don't miss any potential deductions. Pricing: Mint was free (ad-supported) but is transitioning to Credit Karma. Quicken Simplifi is a subscription service, typically around $3-$4 per month when paid annually.

Strategies for Effective Record Keeping and Documentation

No matter how many deductions or credits you're eligible for, they're useless without proper documentation. The IRS requires you to keep records to support the information on your tax return. This isn't just about avoiding an audit; it's about ensuring you can confidently claim every dollar you're entitled to.

Digital vs Physical Records: What Works Best

You can keep records digitally or physically, or a combination of both. Digital records are often preferred for their ease of storage, searchability, and backup capabilities. You can scan receipts, save digital statements, and use cloud storage services. Physical records, like original receipts or important documents, should be stored in a safe, organized manner.

Key Documents to Retain for Tax Purposes

Here's a list of essential documents you should keep:

- W-2 forms (from employers)

- 1099 forms (for independent contractors, investment income, etc.)

- 1098 forms (for mortgage interest, student loan interest)

- Receipts for itemized deductions (medical expenses, charitable donations, business expenses)

- Records of contributions to IRAs or HSAs

- Records of educational expenses (Form 1098-T)

- Bank and credit card statements (especially if you use them to track expenses)

- Records of property sales or purchases

- Mileage logs for business or medical travel

How Long Should You Keep Tax Records

The general rule of thumb is to keep tax records for three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. However, for certain situations, you might need to keep them longer. For example, records related to property you own should be kept until you sell the property and for three years after that. If you underreported income by more than 25%, the IRS has six years to audit you. If you filed a fraudulent return or didn't file at all, there's no statute of limitations. When in doubt, it's often safer to keep records for longer, especially for significant transactions.

Year Round Tax Planning for Maximum Savings

Tax planning isn't just something you do in April; it's a year-round activity. By being proactive, you can make strategic decisions that significantly impact your tax bill.

Adjusting Withholding and Estimated Payments

Review your W-4 form with your employer annually to ensure your tax withholding is accurate. If you're self-employed, make sure your estimated tax payments are on track to avoid underpayment penalties. Tools like the IRS Tax Withholding Estimator can help you get this right.

Reviewing Financial Goals and Tax Implications

As your life changes (marriage, new baby, new job, buying a home), so do your tax implications. Regularly review your financial goals and how they intersect with your tax situation. For example, contributing more to a 401(k) or IRA can reduce your taxable income, while selling investments might trigger capital gains taxes.

Consulting with a Tax Professional

For complex situations, or if you just want peace of mind, consulting with a qualified tax professional (like a CPA or Enrolled Agent) is always a good idea. They can provide personalized advice, identify obscure deductions or credits, and help you navigate tricky tax laws. The cost of their services is often well worth the savings and reduced stress they provide.

By understanding and actively utilizing tax deductions and credits, you're not just filing taxes; you're engaging in smart financial management. It's about being informed, organized, and proactive. So, take the time to explore these opportunities, keep good records, and use the tools available to you. Your wallet will thank you!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)