Restructuring Your Business to Manage Tax Debt Effectively

Explore strategies for restructuring your business operations to better manage and resolve existing tax debt. Learn about legal structures, operational changes, and financial tools to get your business back on track.

Explore strategies for restructuring your business operations to better manage and resolve existing tax debt. Learn about legal structures, operational changes, and financial tools to get your business back on track.

Restructuring Your Business to Manage Tax Debt Effectively

Hey there, business owner! Facing tax debt can feel like a massive weight, right? It's stressful, it's scary, and it can make you question everything about your business. But here's the good news: it's not the end of the road. Many businesses, big and small, have faced tax debt and come out stronger on the other side by strategically restructuring their operations. This isn't just about shuffling papers; it's about making smart, informed decisions that can put your business back on a path to financial health and compliance. Let's dive into how you can effectively restructure your business to manage and resolve that pesky tax debt.

Understanding Your Current Business Structure and Tax Debt Impact

Before you can even think about restructuring, you need a crystal-clear picture of where you stand. What kind of business entity are you currently operating as? A sole proprietorship, partnership, LLC, S-Corp, or C-Corp? Each structure has different implications for how tax debt is handled, who is liable, and what restructuring options are available. For instance, a sole proprietor's personal assets are often at risk, while an LLC offers some protection. Knowing this is your first step.

Next, get a complete understanding of your tax debt. Is it payroll tax debt, income tax debt, sales tax debt, or a combination? Who is the debt owed to – the IRS, state tax authorities, or both? Gather all notices, letters, and records related to your tax debt. This information is crucial for developing an effective strategy. Don't shy away from the numbers; confronting them head-on is the only way to move forward.

Legal Restructuring Options for Tax Debt Management

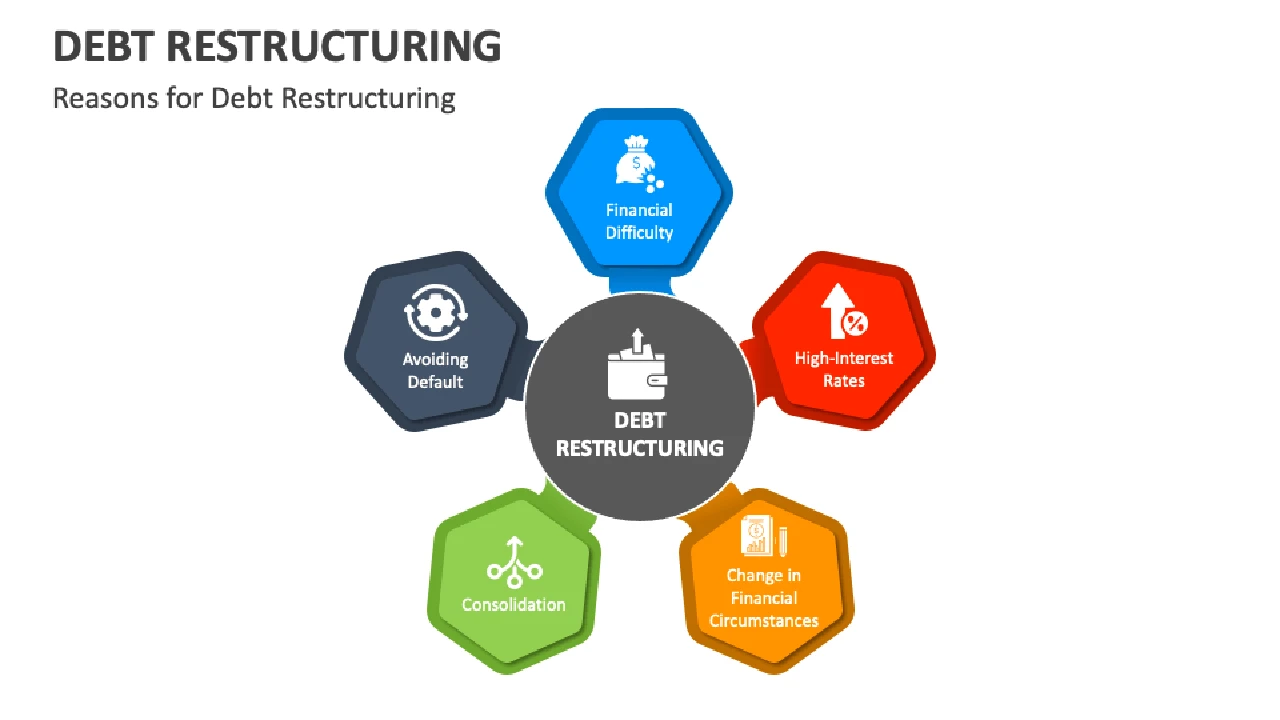

Sometimes, the very legal structure of your business might be contributing to your tax woes or limiting your options for relief. Changing your business entity can be a powerful restructuring tool, especially if personal liability is a major concern.

Sole Proprietorship to LLC or Corporation for Asset Protection

If you're currently a sole proprietor, your personal assets (like your home, car, and personal bank accounts) are not legally separate from your business assets. This means if your business incurs significant tax debt, the IRS or state tax authorities could come after your personal property. Converting to an LLC (Limited Liability Company) or a corporation (S-Corp or C-Corp) can provide a crucial layer of personal asset protection. While it won't erase existing personal liability for certain taxes (like the Trust Fund Recovery Penalty for payroll taxes), it can prevent future personal exposure for business-related debts.

- LLC: Offers liability protection and can be taxed as a sole proprietorship, partnership, or corporation. It's often simpler to set up and maintain than a corporation.

- S-Corp: Provides liability protection and allows profits and losses to be passed through directly to your personal income without being subject to corporate tax rates. This can sometimes lead to tax savings on self-employment taxes.

- C-Corp: Offers the strongest liability protection but is subject to 'double taxation' (corporate profits are taxed, and then dividends paid to shareholders are taxed again). This is usually for larger businesses with plans for significant growth and external investment.

Considerations: This process involves legal filings with your state and potentially the IRS. You'll need to update your EIN, bank accounts, and contracts. It's highly recommended to consult with a business attorney and a tax professional to ensure a smooth transition and understand all implications.

Partnership to LLC or Corporation for Liability Clarity

In a general partnership, each partner is personally liable for the business's debts, including tax debt. This means if one partner skips town or can't pay their share, the other partners could be on the hook for the entire amount. Converting to an LLC or a corporation can clarify liability and protect individual partners' personal assets from business debts. An LLC can be particularly attractive for partnerships as it maintains a flexible management structure while adding liability protection.

Dissolving and Reforming for a Fresh Start

In extreme cases, especially if the tax debt is overwhelming and the business is no longer viable in its current form, you might consider dissolving the existing entity and forming a new one. This is a drastic step and comes with significant legal and financial implications. It's often considered when the existing entity is so burdened by debt that recovery seems impossible, and you want to start fresh with a new business model or a clean slate. However, be aware that dissolving a business doesn't automatically erase all tax debt, especially if personal guarantees or specific tax liabilities (like the Trust Fund Recovery Penalty) are involved. This strategy requires extensive legal and tax advice.

Operational Restructuring to Improve Cash Flow and Reduce Tax Debt

Legal restructuring is one piece of the puzzle; operational restructuring is another. This involves making changes to how your business runs day-to-day to improve cash flow, reduce expenses, and ultimately free up funds to address your tax debt.

Cost Cutting and Expense Optimization for Financial Relief

This is often the first place businesses look. Go through every single expense with a fine-tooth comb. Can you negotiate better terms with suppliers? Are there subscriptions or services you're paying for but not fully utilizing? Can you reduce utility costs, travel expenses, or marketing spend without significantly impacting revenue? Even small cuts can add up over time and create a buffer for tax payments.

- Vendor Negotiations: Reach out to your suppliers. Explain your situation (without oversharing) and ask for better pricing or extended payment terms. You might be surprised at their willingness to work with you.

- Technology Audit: Are you using outdated software or hardware that's costing you more in maintenance or inefficiency? Or conversely, are you paying for multiple software solutions that do the same thing? Streamline your tech stack.

- Energy Efficiency: Simple changes like LED lighting, smart thermostats, or even encouraging employees to turn off lights can reduce utility bills.

Revenue Enhancement Strategies to Boost Income

While cutting costs is important, increasing revenue is often more sustainable. Look for ways to boost your sales and income without incurring significant new expenses.

- Price Adjustments: Have you reviewed your pricing recently? Are you undercharging for your products or services? A small price increase, if justified by value, can significantly impact your bottom line.

- Upselling/Cross-selling: Can you offer additional products or services to existing customers? It's often easier and cheaper to sell more to current clients than to acquire new ones.

- New Product/Service Lines: Is there a gap in the market your business could fill with a new offering? This requires careful market research but can open up new revenue streams.

- Marketing Optimization: Are your marketing efforts generating a good ROI? Focus on the channels that bring in the most qualified leads and sales.

Inventory Management and Supply Chain Optimization

For businesses that deal with physical products, inefficient inventory management can tie up significant capital and lead to waste. Optimizing your supply chain can free up cash and reduce costs.

- Just-in-Time Inventory: Reduce the amount of inventory you hold by ordering products only as needed. This minimizes storage costs and the risk of obsolescence.

- Supplier Diversification: Don't rely on a single supplier. Having alternatives can give you leverage in negotiations and protect you from supply chain disruptions.

- Demand Forecasting: Improve your ability to predict customer demand to avoid overstocking or understocking.

Staffing Adjustments and Workforce Efficiency

This is a sensitive area, but sometimes staffing adjustments are necessary for the survival of the business. This doesn't always mean layoffs; it could involve:

- Cross-training: Ensure employees can handle multiple roles to improve flexibility and reduce reliance on specialized staff.

- Outsourcing: Consider outsourcing non-core functions like accounting, HR, or IT to reduce overhead and gain access to specialized expertise without full-time employee costs.

- Performance Review: Ensure every team member is contributing effectively to the business's goals.

Financial Tools and Products for Tax Debt Management

Beyond internal changes, there are external financial tools and products that can help you manage and eventually resolve your tax debt. These aren't magic bullets, but they can provide necessary liquidity or structure to your repayment plan.

Business Loans and Lines of Credit for Tax Debt Repayment

While it might seem counterintuitive to take on more debt to pay off tax debt, a strategic business loan or line of credit can sometimes be a smart move, especially if the interest rate is lower than the penalties and interest the IRS charges. This can allow you to pay off the tax debt quickly, stopping the accumulation of penalties, and then repay the loan on more favorable terms.

- SBA Loans: The Small Business Administration (SBA) offers various loan programs (like the 7(a) loan or microloans) that can be used for working capital, which can indirectly help with tax debt. They often have more favorable terms than traditional bank loans, but the application process can be lengthy.

- Traditional Bank Loans: If your business has a strong credit history and collateral, a traditional bank loan might be an option.

- Business Line of Credit: This provides flexible access to funds up to a certain limit, which can be useful for managing cash flow fluctuations while you're working on tax debt.

Product Recommendation: For businesses with good credit, Fundbox offers lines of credit up to $150,000 with quick approval. OnDeck also provides term loans and lines of credit, often with faster funding than traditional banks. For SBA loans, you'd typically work with a bank that's an approved SBA lender, such as Chase or Wells Fargo.

Comparison: Fundbox and OnDeck are generally faster but might have higher interest rates than SBA or traditional bank loans. SBA loans offer better terms but require more paperwork and time. Choose based on urgency, creditworthiness, and the amount needed.

Factoring and Invoice Financing for Immediate Cash Flow

If your business has a lot of outstanding invoices, factoring or invoice financing can provide immediate cash. This involves selling your accounts receivable to a third party (a factor) at a discount in exchange for immediate cash. This can be a lifesaver for businesses with cash flow problems due to slow-paying clients, allowing you to pay off urgent tax obligations.

Product Recommendation: BlueVine offers invoice factoring with competitive rates and quick funding. altLINE is another reputable option for invoice factoring, often working with businesses that have larger invoice volumes. Fundbox also offers invoice financing.

Comparison: BlueVine is known for its user-friendly platform and speed. altLINE might be better for larger businesses with consistent invoicing. Fundbox offers a hybrid approach with both lines of credit and invoice financing. The cost (discount rate) and advance rate (percentage of invoice value you receive upfront) vary between providers.

Merchant Cash Advances (Use with Extreme Caution)

A merchant cash advance (MCA) provides a lump sum of cash in exchange for a percentage of your future credit card sales. While MCAs offer very fast funding and are accessible to businesses with less-than-perfect credit, they come with extremely high effective interest rates and can quickly trap businesses in a cycle of debt. They should only be considered as a last resort and with a full understanding of the repayment terms.

Product Recommendation: Companies like Rapid Finance and National Funding offer MCAs. However, due to the high cost, it's difficult to recommend specific products without a deep understanding of your business's unique situation and ability to repay.

Comparison: MCAs are the fastest and easiest to get but are by far the most expensive. They are suitable only for very short-term, urgent cash needs where you are absolutely certain of rapid repayment from sales. Always calculate the effective APR before committing.

Professional Tax Debt Relief Services and Their Role

Engaging with tax debt relief professionals is a form of restructuring your approach to the debt itself. These professionals can negotiate with the IRS or state tax authorities on your behalf, potentially securing more favorable repayment terms or even reducing the amount you owe.

- Tax Attorneys: Best for complex cases, audits, appeals, or when legal action is a possibility. They can represent you in court.

- Enrolled Agents (EAs): Federally licensed tax practitioners who specialize in taxation and have unlimited practice rights before the IRS. They can represent taxpayers in audits, appeals, and collections.

- CPAs (Certified Public Accountants): Can help with tax preparation, financial planning, and some tax debt resolution, especially if the debt stems from accounting errors.

Product Recommendation: For comprehensive tax debt relief, consider firms like Optima Tax Relief, Community Tax, or Tax Defense Network. These companies employ a mix of tax attorneys, EAs, and CPAs to handle various aspects of tax debt resolution. Their services typically include Offer in Compromise, Installment Agreements, Penalty Abatement, and Currently Not Collectible status.

Comparison: Optima Tax Relief is known for its wide range of services and strong customer reviews. Community Tax offers personalized service and a good track record. Tax Defense Network is often praised for its affordability. Always check their BBB ratings and read client testimonials. Prices vary significantly based on the complexity of your case, often ranging from a few hundred to several thousand dollars.

Implementing Your Restructuring Plan and Monitoring Progress

Once you've decided on your restructuring strategies, the key is diligent implementation and continuous monitoring. This isn't a one-and-done process; it requires ongoing attention.

Creating a Detailed Action Plan with Milestones

Break down your restructuring goals into actionable steps with clear deadlines. Who is responsible for each task? What resources are needed? For example, if you're changing your business entity, list all the legal filings, bank account updates, and communication with stakeholders. If you're cutting costs, set specific targets for each expense category.

Regular Financial Review and Adjustment

Set up a schedule for regular financial reviews – weekly, bi-weekly, or monthly. Monitor your cash flow, profit and loss statements, and balance sheet. Are your cost-cutting measures working? Is revenue increasing as expected? Are you making progress on your tax debt payments? Be prepared to adjust your plan as circumstances change or as you gain new insights.

Communication with Stakeholders and Tax Authorities

Transparency, where appropriate, can be beneficial. Keep your employees informed about the changes and why they're necessary. Communicate with your suppliers and creditors if you need to negotiate terms. Most importantly, maintain open and honest communication with the IRS or state tax authorities. Ignoring them will only make things worse. If you're working with a tax professional, they will handle this communication for you.

Building a Strong Financial Foundation for the Future

Restructuring isn't just about fixing past mistakes; it's about building a more resilient business for the future. Once you've addressed your tax debt, focus on establishing strong financial habits:

- Emergency Fund: Build a business emergency fund to cover unexpected expenses or future tax obligations.

- Regular Tax Planning: Don't wait until tax season. Engage in year-round tax planning with a professional to optimize your tax strategy.

- Robust Record-Keeping: Implement excellent accounting and record-keeping practices to avoid future discrepancies.

- Cash Flow Projections: Regularly project your cash flow to anticipate future needs and potential shortfalls.

Restructuring your business to manage tax debt is a challenging but ultimately rewarding process. It requires courage, strategic thinking, and often, professional guidance. By understanding your options, making informed decisions, and diligently implementing your plan, you can navigate through tax debt and emerge with a stronger, more financially stable business ready for future success.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)